I’m investing for both of my kids and if I continue with my currently strategy they will be millionaires in their forties. Let me share more about how to invest for your kids!

If you want to set your kids up financially, investing early on their behalf is one of the best things you can do. Plus if you are based in the UK, investing for your kids in a JISA protects their savings (& growth) against tax.

What is a JISA?

JISA stands for Junior Individual Savings Account which is a tax advantaged savings account. You can save up £9,000 a year in a JISA tax-free. Meaning you don’t pay any tax on the growth, either from interest or from investing the money into the stock market.

Parents/Guardians can open the account on behalf of their child but the funds are locked until the child turns 18. When it will automatically convert from a JISA to an adult ISA, where it could continue to grow tax-free.

There are two different types of JISA, cash and stocks & shares. Typically cash JISA’s will have an interest rate attach to it where as with a stocks & shares JISA, you can pick investments to put the funds into. You can hold one of each account in your childs name but the £9,000 threshold is a combination of the two. So it’s not £18,000 if you have one of each.

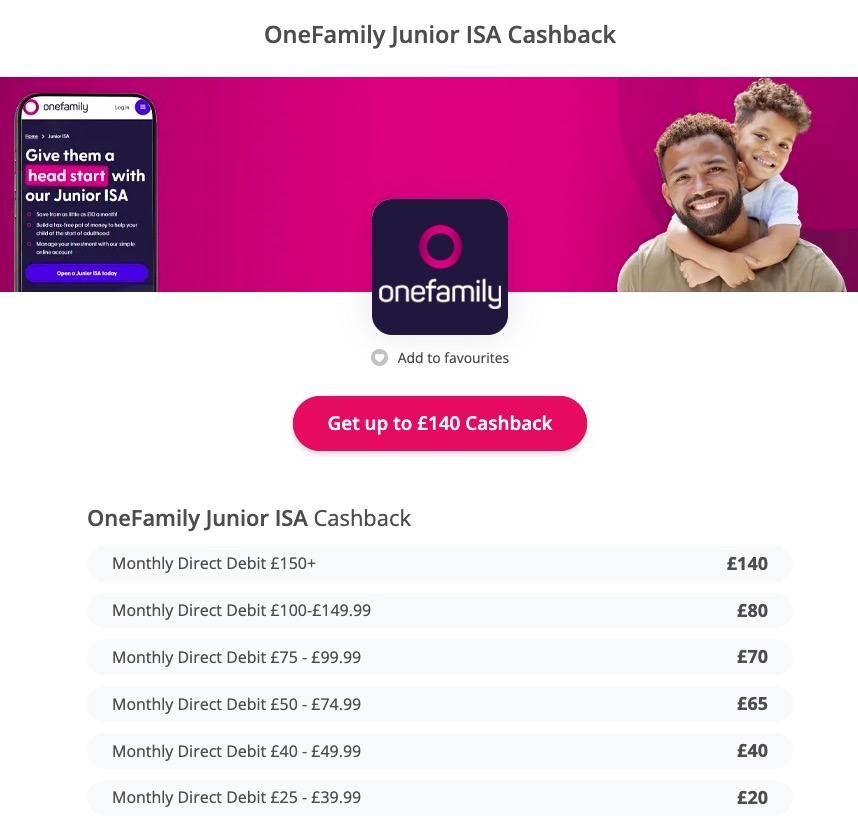

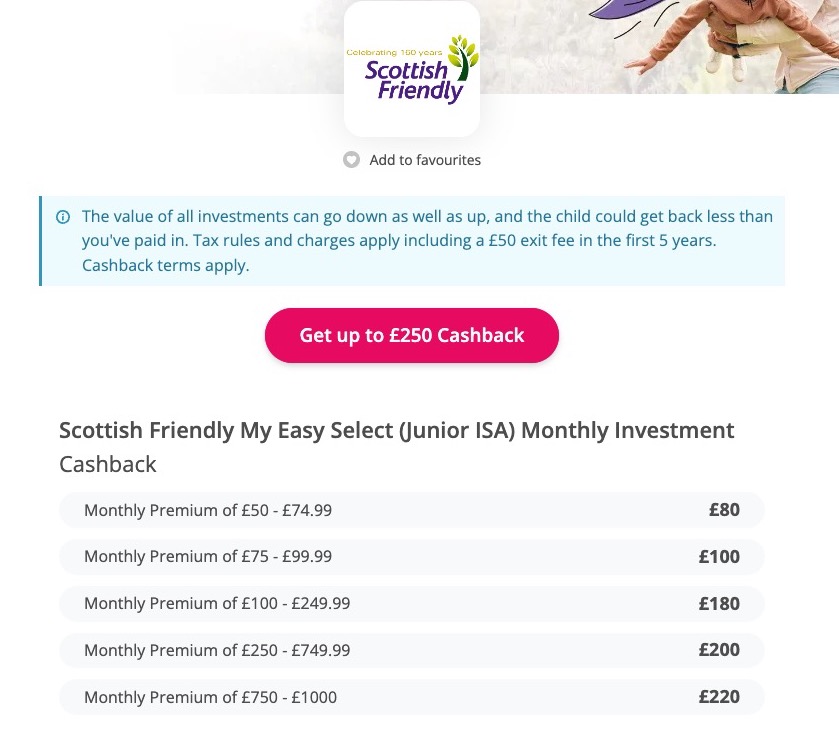

Now, I wouldn’t be The Savvy Spender if I didn’t encourage you to shop around and get cashback when opening a JISA for your little one. TopCashback has a handful of good offers for Junior ISAs. Here’s a couple I found from a quick browse.

That’s up to £220 in free money for setting up the JISA through TopCashback. Browse more offers and sign up to TopCashback here.

Why investing for your kids is important?

No matter how much or little you can invest for your children, starting early is the best gift you can give them.

This is why we have chosen to use Stocks & Shares JISA’s instead of cash JISA as historically you can get a higher return from investing than the interest rate offered.

Kids have the biggest advantage when it comes to investing and growing their money… time! As adults, investing is still super important but we have less time on our side so we don’t benefit from the power of compound interest as much as they will.

The Power Compound Interest

Compound interest, famously described as a the eight wonder of the world by Albert Einstein is the snowball effect that happens when your money starts to earn money. When you invest or save your money you will often earn interest which will compound overtime, exponexically growing your money.

It is the power of compound interest that we need to tap into for our kids savings. Let’s look at a case study of what would happen if you invested your child benefit money each month. You will really be able to see the power of compound interest in action.

Case Study: Child Benefit Millionaires

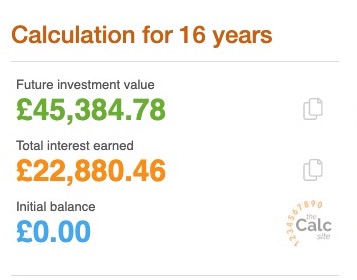

Parents in the UK can get up to £27.05 per week in child benefit. This is the rate for a first child to parents who earn under the income threshold of £60k. Over a year this is £1406.60 and is currently available until your child turns 16 or 20 if they stay in education.

Let’s assume that the benefit stays at £27.05 per week for the entire 16 years and you invest every single penny for your child in a tax-free JISA.

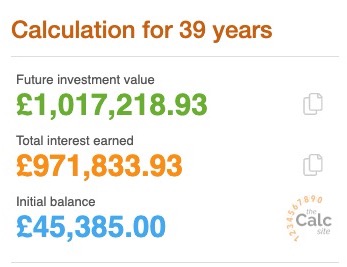

After 16 years you will have contributed £22,505.60 and assuming an 8% return, the account could be worth over £45k. If you then stopped contributing and didn’t withdraw a penny, the investments would continue to grow. Assuming an 8% annual return, that £45k could grow to over £1,000,000 after 39 more years.

Meaning that by simply investing your child benefit money which is “only” £27.05 a week, your child could be a millionaire by the time they are 55 without lifting a finger. Now that’s a pretty nice inheritance!

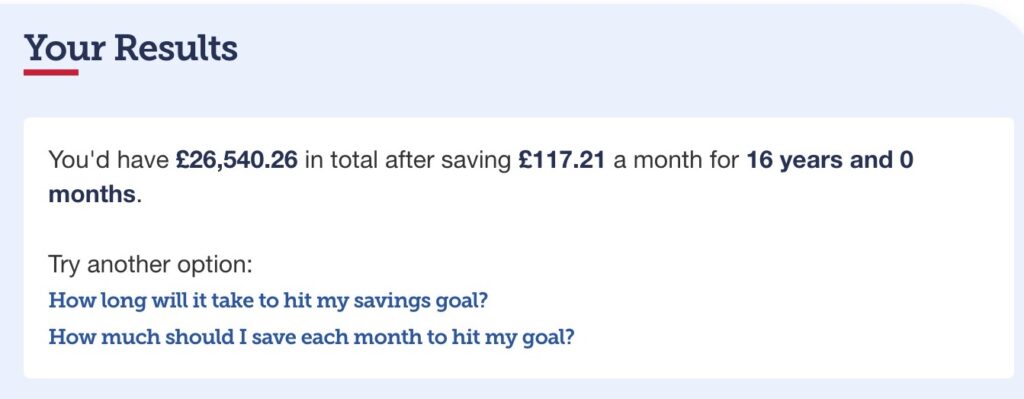

On the flip side, if you didn’t invest the money and instead put it into a cash savings account earning a simple interest rate. Simple interest is different from compound interest in that you won’t earn any money on the interest you earn. So the money will grow slower and typically cash savings accounts historically have a lower rate of return than the stock market. Let’s assume you save the entire £27.05 weekly child benefit into a savings account earning 2%.

After 16 years you’d have £26,540.26 in the account which is an increase of over £4k which is good but nothing compared to the increase of almost £23k if you invested that money. That’s the power of compound interest!

My Strategy

Every month we send their child benefit into their Stocks & Shares JISA plus a set amount each month as a standing order. Both of our children are commercial models so any money they make from jobs also gets invested. We also send any money they get from birthdays or christmas to their JISA’s too.

Not factoring in any variable income (modelling or presents) both our girls should have £100k in their JISA’s by the time they are 16. This is assuming an 8% yearly return on the investments.

If they don’t invest another penny but keep that same amount invested, by the time they’re 46 they will have over £1,000,000 in their investment accounts. Again this is assuming an 8% return rate. And that is the incredible power of compound interest!

Whilst we know a million pounds won’t be worth what it is now in 40+ years, it’s a lot better than nothing! On top of investing for our kids, we also know the importance of passing on financial knowledge and education to them as well.

I hope you now have a solid idea of how to invest for your kids and this article has given you something to think about. Have you thought about investing for your kids before? What strategy have you decided on? I’d love to hear more in the comments!